Why History Repeats Itself

I find myself returning to the topic of our magnificent financial machinery once more, and I must say that my reasons are not entirely wholesome. Pour yourself a drink for this one, and try to stay in a relaxed state of mind while I unwind some seriously unpleasant stuff.

Previously, on ‘As the Hedge Fund Turns…’

When we last talked about this, we discussed how large Wall Street firms with infinite money, complex software, a smattering of sleight of hand, and a complete dearth of decency can control and bend the price of certain stocks to their will. This is usually done to profit off short selling. To be perfectly fair, short selling is not necessarily evil. It’s a dirty, ugly business, sure. But it actually serves a viable purpose when applied judiciously. The ability to short sell a falling stock provides liquidity to the market and stabilizes the prices. It exists to allow investors to ‘hedge’ against bleeding capital when a stock is plummeting. They can make money when it’s coming up, and they can make money when it’s going down, too. When you settle the ups and downs at the end of the day, investors and markets probably lost less than they might have at the cost of gaining less than they might have. It blunts the effect of volatility.

This is good, until it goes bad. It goes bad when morally bankrupt assholes who see only dollar signs get a hold of it and begin to min/max the system like a coked-up DnD nerd.

Here’s what happens. Companies and stocks that are struggling get shorted, and the shorters then attack the stock vigorously to drive the price as low as possible. Even unto the destruction of the shorted company, which is the ultimate jackpot for the shorters. A short seller does not have to repurchase (cover) shares that don’t exist anymore, making the profit on the short sale 100%. This was what we discussed last time.

What’s Happening Now?

The phenomenon of the “Short Squeeze” and “Meme Stocks” has birthed a movement. The same group of rabid retail investors (poor people) on Reddit who figured out how to squeeze a shorted stock through the complex tactic of buying it at market price and refusing to sell have been on a tear. Assembling large numbers of nerds and directing them at a hated target is the sort of magnificent clusterfuck that single-handedly justifies the existence of the internet. Never in human history have so many staggeringly incompetent people set their minds to a task to such glorious effect. Never underestimate the power of angry nerds with nothing better to do.

High finance is an indecipherable mess of jargon, fuzzy math, legal loopholes, and deliberately obfuscated reporting. It’s more than just hard to understand, it is, by its very design, impossible to understand. It is the mutant offspring of economic theory, legal theory, computer science, game theory, human psychology, and old-fashioned carny hucksterism. A person can master a few aspects of it, but no one really sees the whole thing at once. It takes hundreds of very smart people to make a large Wall Street firm function, often thousands.

But just ask the ancient Egyptians, Romans, Byzantines, Mongols, Vikings, and Visigoths about the power of numbers. They will tell you that almost anything that can be accomplished by a few very smart people can also be accomplished by a larger number of average people, or even an enormous horde of morons.

The hordes of Reddit mobilized, and the veil of mystery protecting the intricate financial machinery of Wall Street soon collapsed beneath a Mountain Dew-fueled wave of weaponized nerdery.

Much of what was found turned out to be useless. Much of it was misunderstood. Many conclusions were incorrect. Most of the searchers barely even understood what they were looking at when a document or a filing was discovered. This did not stop anyone, though. The internet needs neither knowledge nor understanding of a topic to form firm opinions about it, after all. Hundreds of posts appeared with fuzzy images of financial statements, screenshots of balance sheets, graphs, and rambling data dumps. The discussions ran the gamut between serious investigations and mere excuses to hurl memes. The democratization of data is a marvelous unfiltered mess. This is never more apparent than on an internet message board.

They’re Evolving!

Then… oops! The idiots began to learn. If you put two-hundred-thousand eyes on anything for any length of time, stuff will get noticed. People discussing the issues develop deeper understandings and comprehension improves. Soon enough, patterns began to emerge between a few key financial players. Connections that were not obvious before became starkly apparent. Questions were asked, and wiser minds on other platforms answered those questions. After months of learning, growing, evolving, the hive mind of amatuer internet investors made a few startling discoveries.

The world’s financial institutions and the machinery of commerce are at the mercy of a few bad apples. That’s the bad news. The good news is that their bullshit is getting harder and harder to hide.

Canaries in Coal Mines

Canary #1: New Rules Blues

On March 18th, the DTCC issued new rules about a few things. What’s the DTCC? Imagine you want to buy a car from some random guy on the internet. You want some protection from the chance that the car advertised may not even exist (like some shares of stocks don’t actually exist when you buy them). So, you give the cash to a third guy (the DTCC) who holds on to the money until the car is delivered. The seller gives the car to the DTCC and the DTCC ensures that it is the right car and that you have deposited the correct amount of money. If everything is groovy, the seller gets the cash and you get your new whip. This is called “settlement” and the DTCC takes a fee for being the intermediary.

The DTCC is not a government agency, and they operate under rules that they set and stick to. The biggest upcoming rule change (SR-NSCC-2021-801), which has yet to be approved, allows the DTCC to liquidate member positions in the event of a default. That’s a fancy way of saying, “If we think you are being too reckless, we’re going to sell all your shit to cover your stupidity.” This rule has been a long time coming, because the DTCC was notoriously silent on the financial shenanigans that caused the 2008 financial crisis. Shenanigans it appears the DTCC knew about and turned a blind eye to. Imagine that.

A second new rule, (SR-DTC-2021-003) effective immediately, clears up some ambiguity in short-position reporting requirements. Previously, because the rules were written in crayon by a drunk walrus, funds were only reporting their short positions every 30 days. Often, the information reported was for the preceding month, making the reports 60 days in arrears the moment they hit the books.

Remember kids, trades can be made THOUSANDS OF TIMES PER SECOND. How helpful is 60-day old news in that environment? At any given moment, there was no way to tell the quantity of short positions a fund had on the books. This is important stuff to know if you are the agency responsible for ensuring the transactions go through. A fund with too many short positions, or as in the case of AMC and GME, holding VERY BAD short positions, is at serious risk for a “short squeeze.” The losses to that fund can be devastating, causing the fund to default and leave the DTCC holding the bag. The new rule says that a fund must disclose its current positions at any time the DTCC asks. And believe me, the DTCC is going to ask. The scrutiny they suffered under in 2008 left a bad taste in their collective mouths.

But why change the rule now? Why not in 2008? Well, because the 2008 crash was due to risky mortgage-backed securities, and not (necessarily) short-selling. The DTCC smells a similar meltdown coming because of naked short-selling, and they want to be clear of the shrapnel when it all blows up. Make no mistake though, this is the same setup as before, just with different collateral.

Let me reiterate the important bit: the agency that physically completes 90% of all securities transactions is suddenly taking bold steps to protect itself from another version of the 2008 market crash…

Canary #2: The REPO man cometh…

Not that kind of repo man. The REPO man. REPO in this case refers to a special kind of transaction called a “repurchase and reverse repurchase agreement.” It’s like a pawn shop for stocks, bonds, and other transferable securities. If you need cash, you just take your stocks down to the REPO man and swap them for cash. Your stocks are collateral on a quickie loan you use to try to make more than the interest the REPO man is charging you. If you do it right, the borrowed money makes a healthy profit even after paying interest. If this sounds like pawning the family jewels to bet on a horse race, then you are understanding it correctly.

Wall Street hedge funds LOVE these things. They provide tons of instant liquidity for quick moves, and the interest is not terrible if you don’t let the loan stretch out too long. If you default, the bank keeps your collateral.

But what if your collateral is garbage? This is what happened to Lehman Brothers in 2008. They borrowed money against low-quality mortgage-backed securities they had mis-labeled as “sales” to hide the risk. We know what happened next.

Now the new REPO hotness is the 10-year treasury bond. Lenders like it as collateral because it’s really freakin’ reliable. Problem solved, right?

Wrong.

The bastards have been shorting the 10-year treasury bond almost as badly as they have AMC and GME. Treasury bond prices have been declining steadily as a result. That’s not good if you want to use it as collateral…

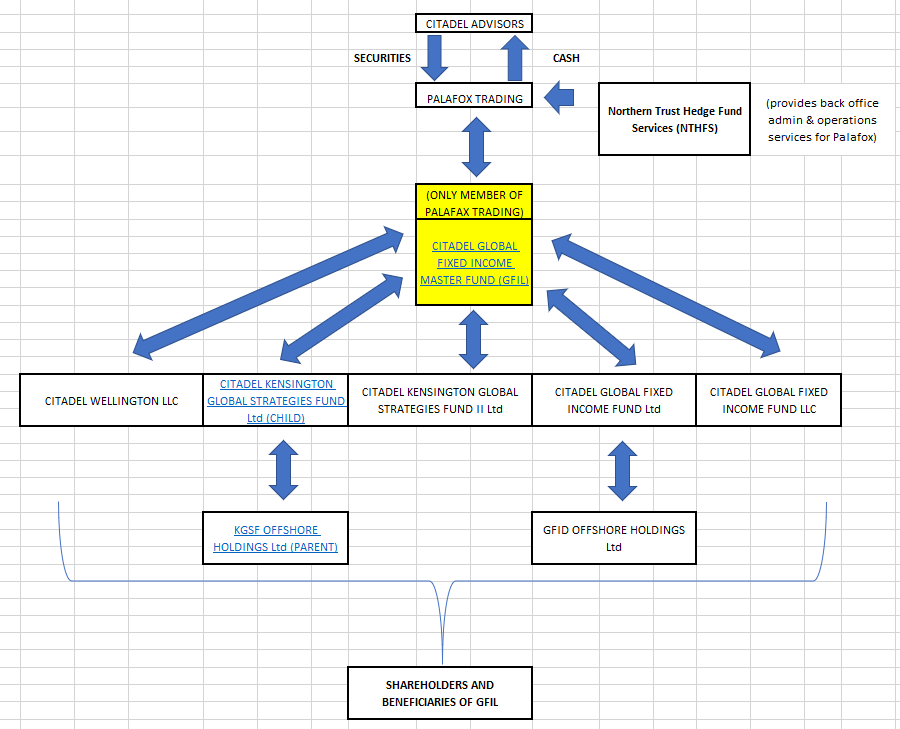

99% of the $31 BILLION in treasury bonds held by Palafox Trading are tied up in REPO agreements for super-mega-hedge fund Citadel Global. But get this… Citadel OWNS Palafox. Palafox secures treasury bonds, swaps them for cash, and then loans the cash to Citadel. It’s not that complicated. Just look at this helpful diagram from redditor u/atobitt:

This starts to get a little dark. 80% of Cital Global’s $123 BILLION then disappears into the Cayman Islands before returning as investments or… not. Not a joke. Not bullshit. It’s all legal and in their own filings.

How do we know that treasury bonds are drying up? At three separate points in the last year, the REPO rate for treasury notes was negative %4.25. That means REPO market makers were PAYING borrowers 4.25% to borrow money. WHY? Because the borrowers were putting up treasury notes as collateral, and there were not enough notes on the market to cover all the shorts. Why not? Because they were now worth less because of all the shorting.

Wait. Does that mean that hedge funds have shorted more treasury notes than are available to buy?

Yes.

Isn’t that just another kind of short squeeze?

Sure is.

Is Citadel the same company that holds a major stake in RobinHood, and has shorted AMC and GME beyond what is even available to cover?

That’s them.

What happens when Citadel has to cover all of these crazy positions?

They will have to liquidate pretty much everything, triggering sell-offs in other stocks and likely causing a massive cascading crash in stock prices worldwide.

But don’t worry, they’ll pull every dirty trick they know to prevent that from happening.

Canary #3: The Fall of Archegos

Archegos Capital Management was a “family office” fund. It escaped most legal and regulatory scrutiny because it managed a single fortune and did not take on investors. Sounds nice. Well, not in this case because the “family” in question was Bill Hwang. Hwang is a particular type of Wall Street predator, a sort of ethically barren clearing house for greedy ideas unencumbered by the weight of morality. His original firm, Tiger Asia Management was dissolved after getting caught doing literally every illegal financial thing. Banned from ever working in the Financial sector, Hwang set up a modest office to manage his personal fortune. Except his personal fortune was made up of GINORMOUS lines of credit from such brilliant lenders as Credit Suisse, Nomura, Goldman Sachs, and Morgan Stanley. Why did these reputable companies agree to hand mountains of cash to a guy famous for being a liar and a thief? Some say they believed in the power of redemption. Some say they refused to let the past define his future. Others imply that the millions in management fees they were getting paid made all other thoughts crumble. All those ethical and legal objections collapsed into a fine white powder not unlike that which a wealthy jerk might snort from the cleavage of an expensive escort. Who can say what they were thinking, really?

Anywho, Hwang used this money to make leveraged bets on a bunch of stocks using a system called “total return swaps.” This meant that Hwang did not actually own any of the stocks in question, and the sellers did not know they were dealing with a notorious con man. Otherwise, he’d have been tossed out on his kiester. Naturally Hwang’s new banking besties made sure no one was the wiser.

Hwang is a pretty good con man, but it turns out he is a mediocre investor at best. When the stocks began to fall, Hwang’s positions relative to how much he had borrowed to get them started to look very bad. His lenders, seeing their money disappear like the aforementioned white powder, suddenly remembered that Hwang was a lying asshole. In a sudden burst of social responsibility, they decided to sell his stocks to get their money back (before it was all gone). This pretty much killed Archegos and revealed to the world that a known scumbag had been sneaking his way into markets right under everybodies’ noses. Archegos held large positions on leverage that when liquidated triggered sell-offs in other areas. Credit Suisse and Nomura lost a total of $5.2 billion combined.

One dishonest con man did that. One. You figure he’s the only one?

Who’s in Charge Here?

The inmates have taken over the asylum, people. Our regulatory agency, the SEC, has not had meaningful control over hedge funds in decades. Both the Republicans and Democrats have failed miserably in fixing this, and who can blame them? The sheer wealth and power of Wall Street exerts enormous influence over our politicians in the form of billions spent on lobbies and donations. If Wall Street was a monolithic entity it would not be so bad. It would act in its own self interests and destructive behaviors like naked short selling and price manipulation would be rare. But Wall Street is composed of competitive entities whose only goal is profit every quarter. For far too many of these, the damage they cause the greater marketplace is irrelevant so long as they keep those profits soaring.

It’s the prisoner’s dilemma: If everybody works together, the results is sub-optimal for the individual but better for the group. If some fuck over the others (naked short-selling, colluding, etc.) then they succeed at the expense of the group. If everybody misbehaves, the outcome is bad for everybody.

We are at the ‘everybody is an asshole’ phase right now. The whole market is risking another meltdown a la 2008 and it’s for the exact same reasons. Whether you call it “margin” or “leverage” or “REPO,” everybody is making too many wild bets with borrowed money. At some point the debts have to be paid, and it’s a frantic scramble to see who gets stuck holding the bag. A bunch of those bets got called this week, and a few of the game’s most recognizable players were left holding and looking like fools. DTCC is acting like it expects more to follow. These are not good omens, folks.

But there is hope.

What is really rattling the hedge funds these days is the rise of the retail investor. A retail investor is a (poor) person who buys and sells stocks on a very small scale for personal reasons. If you use Robinhood or Stash or Webull, you are a retail investor. Retail investors have power for two reasons.

1: They buy with actual money. Not collateralized debt, not swaps. Cash in, cash out. Stable, reliable, instantaneous. Cash is king and the retail investor will accept nothing else. When the little guys are holding the asset (stock) and they will only part with it for cash, it creates a bottleneck in a system that has evolved to move debt. If you want that asset, then you must pay for it at the price the retail investor sets. They aren’t paying interest, or forced to have collateral. The only time the retail investor takes a loss is if they sell below the price they bought at.

2: The retail investor can afford to lose. So many of the games played on Wall Street are built around collateralizing debt, avoiding interest, and finding new ways to shift the enormous risks leverage engenders. The retail investor ignores all of that. The money spent on a stock is gone until the stock is sold. Life goes on. The retail investor has no access to that liquidity anyway, so it is not catastrophic if the stock drops or if it needs two decades to recover. Hedge Funds that dip too deeply into the gray areas of legality and leverage cannot afford to lose. They become desperate and do things like borrow more shares and short them just to cover their previous shorts. Then you get short squeezes like we are seeing now.

In the meantime, the failures of the SEC should probably be addressed. The most egregious shortfall being the structure for fines and the lack of criminal prosecutions. Fining Citadel $275,000 for misreporting one quarter is ludicrous in the face of the hundreds of millions in profit they made. That’s less than their coffee and caviar budget. It’s not a punishment, it’s a line-item expense.

Why is Bill Hwang not in jail? THEY PUT MARTHA STEWART IN JAIL FOR LESS. In total, all the fines levied by the SEC against the worst actors in the 2008 crash do not add up to 1% of the cost of bailing the country out. No one went to jail. The list goes on, but the refrain is always the same: Multibillion-dollar fund pays a few million in fines and goes on its way. This is not a disincentive to bad behavior, it’s a small tax on getting caught.